I’m old school, and I like my dividends.

In my view, dividends are almost inconsequential these days compared to the returns realized from rising stock prices.

Since bottoming out in early 2009, the S&P 500 has exploded higher at a compound annual growth rate of over 15% per year and is up over 300% cumulatively.

What’s a couple percent in dividends when you’re looking at those kinds of capital gains?

Dividend Math

Furthermore, very few sexy, high-growth tech companies pay dividends. Amazon (AMZN), Facebook (FB), and Alphabet (Google) certainly don’t, and none have immediate plans to start.

But I think it’s important to keep a few things in mind. To start, the 15% annualized returns we’ve seen over the past decade in the S&P 500 are by no means normal. The long-term term historical average is closer to 10%.

And mean reversion being what it is, having a long period of above average returns means we need to have a long stretch of lower-than-normal returns to get us back to the long-term average.

In my view, not even the glassiest-eyed permabull seriously believes returns of 15% per year can continue forever.

Purchase Price

The returns you achieve are ultimately a product of the price you pay. When you buy them cheaply, you put yourself in position to enjoy higher-than-average returns. When you overpay, you set yourself up to be disappointed.

The S&P 500 currently trades at a cyclically adjusted price/earnings ratio of 29.9. That implies it is priced to deliver losses of about 2% per year over the next eight years, assuming the market returns to its long-term average valuation.

Now, maybe we get lucky and valuations remain at historically elevated levels.

Stay Realistic

But even assuming valuations remain 25% to 50% higher than their long-term averages, we’d still be looking at returns in the ballpark of just 1% to 3% per year.

When you’re used to making 15% per year, making 3% (or even losing money) is a bitter pill, particularly if you’re already in retirement and have to take portfolio drawdowns.

This brings me back to dividends.

Dividend Power

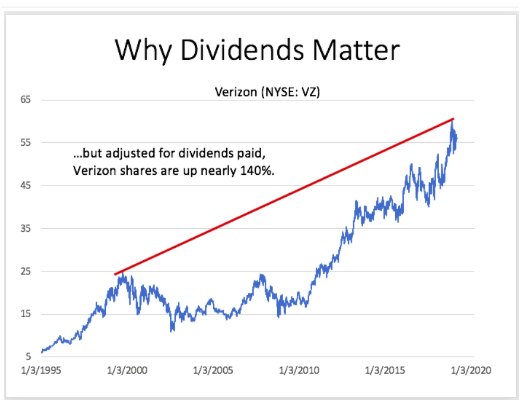

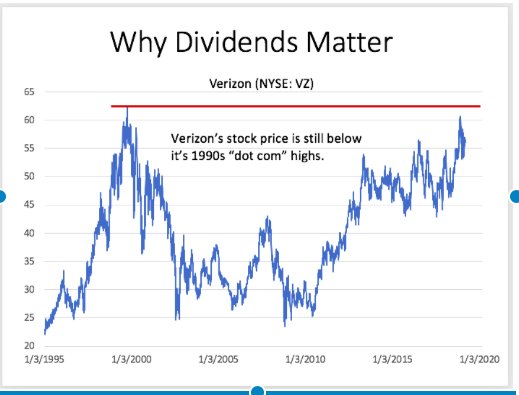

Take a look at the following two charts. The first is a standard price chart of telecommunications giant Verizon (VZ).

Nearly 20 years since the peak of the 1990s internet bubble, Verizon has yet to see new highs. Had you had the remarkably bad timing of buying Verizon at its 1999 high, you’d still be under water two decades later.

Now take a look at the second chart. This is also Verizon, but this chart adjusts stock prices to account for dividends paid. For most of the past 20 years, Verizon has sported a dividend yield of between 4% and 6%.

Takeaway

Suddenly, I think Verizon doesn’t look so bad. Even buying one of the most overpriced major stocks at the peak of the biggest stock bubble in history, you still would have enjoyed total returns of more than 140% after accounting for Verizon’s massive dividend yield.

In my view, you can’t always depend on capital gains. In my opinion, when you focus on dividends, you don’t have to worry as much about capital gains.

Photo Credit: Pictures of Money via Flickr Creative Commons