By Steven Levine, Senior Market Analyst, Interactive Brokers

The U.S. auto industry has been recently beset by a long list of headwinds, including global trade disputes, rising commodity prices, as well as weaker emerging market currencies.

U.S. auto giants Ford Motor Company (F) and General Motors (GM), for example, have generally blamed tariffs and adverse foreign exchange fluctuations for dents in their latest quarter’s earnings results.

Challenging Times

Ford CFO Robert Shanks admitted during the company’s Q2’2018 earnings call that the quarter was “challenging,” due in part to an “increasingly uncertain” policy environment that’s “causing real unfavorable bottom line effects on the business such as higher commodity cost beyond normal cyclical effects as well as tariff-related impacts.”

Ford’s revenue, net income and adjusted EBIT were all down year-over-year in Q2’18 mainly driven by factors related to a North American production disruption at a parts supplier in the quarter, as well as ongoing challenges in the China market.

The firm’s revenue slipped by US$1.2bn from the same year-ago quarter to US$35.9bn, while its EBIT margin contracted by 3.3 percentage points to 3.2%. Furthermore, local Chinese market sales plunged in August by 36% year-on-year, and down 27% since the start of the year.

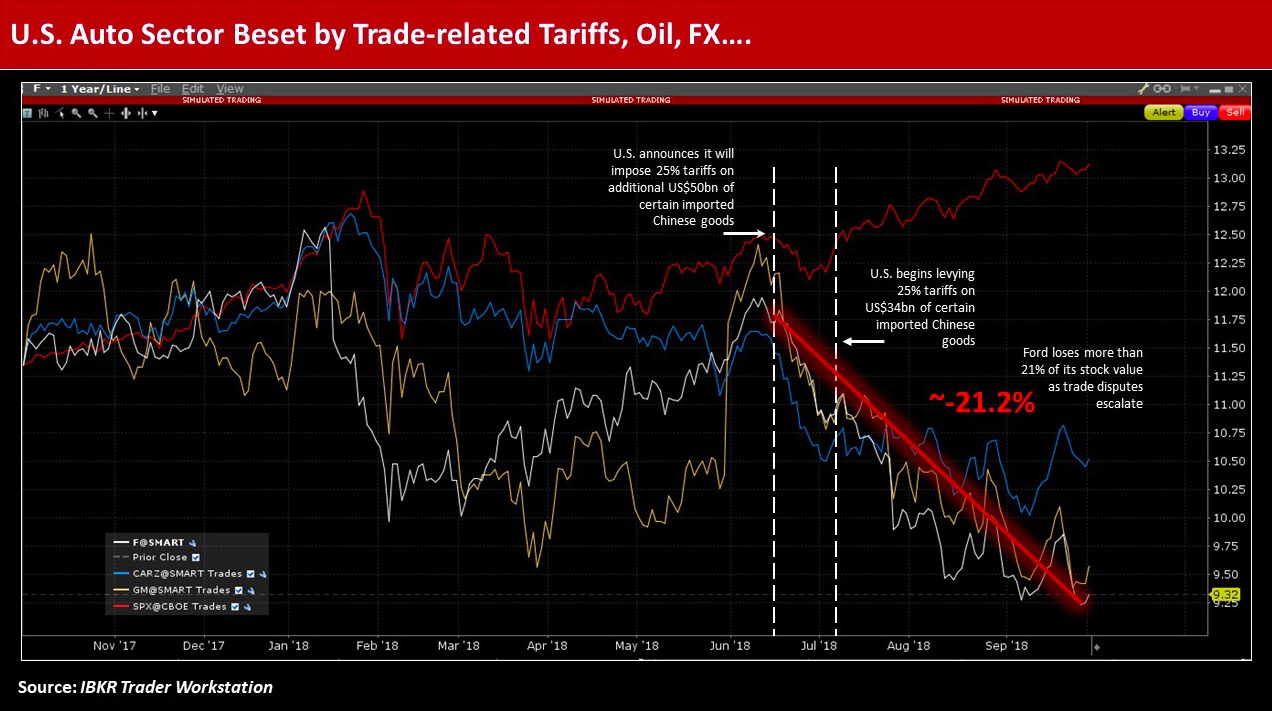

Slumping Stock

Against this backdrop, Ford’s stock has slumped more than 21% since the Office of the United States Trade Representative (USTR) announced in mid-June the imposition of an additional 25% duty on around US$50bn worth of Chinese imports containing what it deems as “industrially significant technologies,” including those related to China’s “Made in China 2025” industrial policy.

The USTR’s action, related to its Section 301 investigation, was ultimately issued in two tranches – one in early July on US$34bn worth of goods and the remainder finalized in early August.

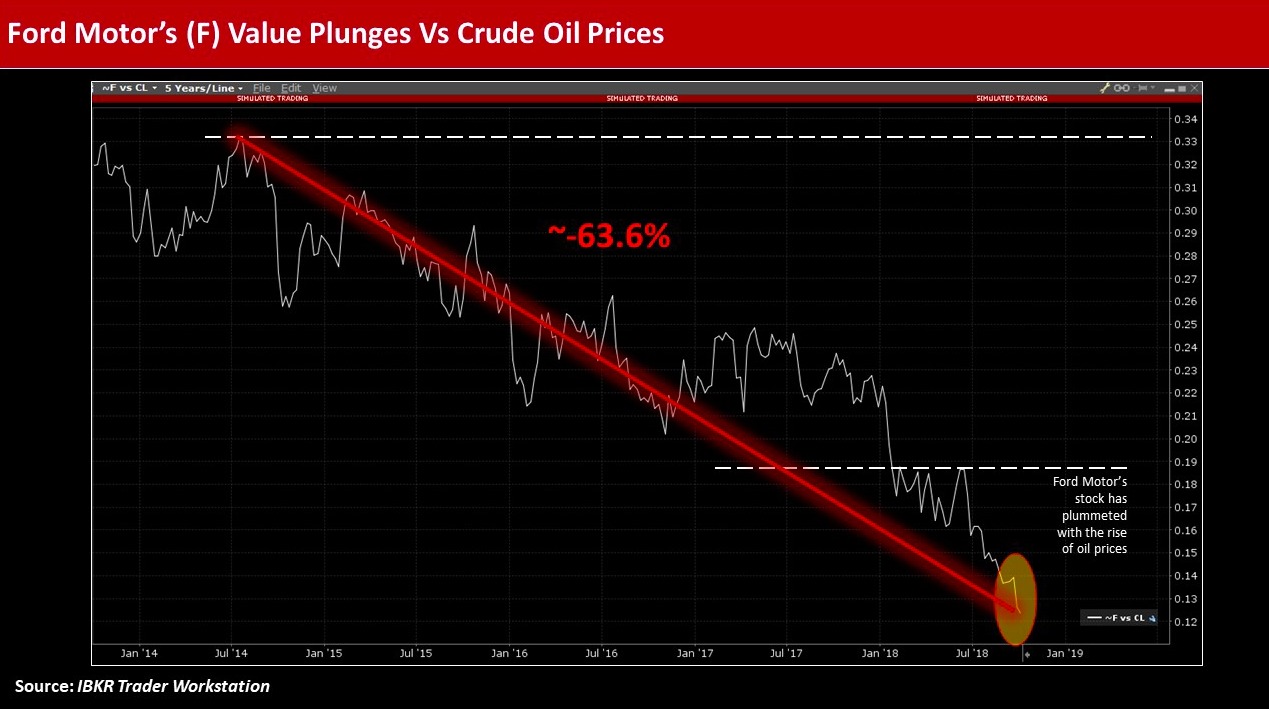

Ford’s shares have also fallen a little more than 30% since its 52-week peak set in mid-January, while its bondholders have generally grown increasingly nervous about its credit profile.

Debt Worries

Over the past three months, the perception of the carmaker’s ability to repay its debt obligations has eroded, with the spread on its 5-year credit default swap (CDS) recently quoted wider by almost 32.5bps at just north of 170.5bps.

The yield on the company’s 6.625% notes due October 2028 have risen roughly 118bps since late February to 5.936%, according to the IBKR Trader Workstation.

GM Headwinds

General Motors CFO Chuck Stevens recently said GM’s operating performance was “impacted by significant headwinds from commodity costs and currency devaluations in South America.”

In Q2’2018, GM said higher prices of commodities and unfavorable foreign exchange impacts from the Argentine peso and Brazilian real had negatively affected its business expectations.

As the company anticipates these foreign exchange headwinds will continue through the second half of 2018, it revised its full-year outlook, including a 9.37% year-on-year drop in its diluted-adjusted EPS to around US$6.

Price Slide

GM’s shares have fallen nearly 28% since its 52-week high set in late October 2017, while its bondholders also have some jitters about its credit profile.

However, the perception of GM’s ability to repay its debt obligations over the past three months has been less severe than Ford’s, with the spread on its 5-year CDS recently quoted wider by nearly 7bps at just south of 131.5bps.

The yield on the company’s 4.2% notes due October 2027 has risen roughly 68 bps since late February to 5.031%, according to the IBKR Trader Workstation.

Emerging Markets

The recent rise in the U.S. dollar has created challenging conditions for many emerging market (EM) countries, including increased debt servicing costs as their local currencies slide, as well as higher commodities prices, and more expensive U.S. exports.

Analysts at Rareview Macro pointed out that typically currencies with large current-account deficits should depreciate relative to those of countries with surpluses. They noted this will “stimulate their exports and curb imports, thereby helping to slim the trade gaps.”

Rareview Macro said that to date, the currencies of Turkey, India, Argentina, Brazil and Mexico fall into the “Bad EM” bucket, while those of China, Malaysia, Thailand and South Korea comprise the “Good EM” category.

They added the list could go on, “but until crude stops appreciating, Indian risk assets remain a key liability in emerging markets.”

Meanwhile, the Fed’s ongoing tightening of monetary policy has generally exacerbated conditions, with its latest rate hike preceding key central bank rate decisions in the Asia-Pacific region in the week ahead, including from the Reserve Bank of India (RBI).

Upside Potential

Although the auto sector faces numerous additional threats, including an expected increase in the cost of crude oil from U.S.-imposed sanctions on Iran, as well as the potential for higher U.S. interest rates as the Federal Reserve continues to tighten monetary policy, some analysts continue to wax optimistic about the auto sector in the near-term.

Moody’s Investors Service analyst Falk Frey recently noted that global auto sales to date this year continue to support his full-year 2018 forecast, while greater downside risks that appear to be emerging could hurt sales next year.

He cited that these headwinds include trade and tariff disputes, rising interest rates and higher fuel prices.

Frey added that steady auto sales in China are a key driver of his global forecast, “but growth will remain far more modest than the double-digit percentage gains seen as recently as 2016.”

Sales Outlook

Moody’s anticipates that global light vehicle sales will grow 1.5% this year and 1.3% in 2019, while auto sales in China are expected to rise 2% this year – slowing from 3% in 2017 – then edge up to 2.5% in 2019.

Meanwhile, Moody’s said U.S. light vehicles sales will likely cool in the coming months, as rising interest rates, “higher vehicle prices and the threat of tariffs on auto imports are likely to make consumers consider a used car or delay buying a new one.”

Moody’s also noted that although U.S. light vehicle sales are expected to fall by 1.2% in 2018 and 0.6% next year, they will remain strong relative to historical levels and are on track to reach 16.9 million units this year.

Photo Credit: Mike Mozart via Flickr Creative Commons

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by Interactive Brokers or Interactive Brokers Asset Management to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice. Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}