The first quarter of 2018 was not kind to value and income investors. Long-term bond yields started rising in the second half of last year, and that trend accelerated in January. For the quarter, the Dividend Growth portfolio lost 7.36% (net of fees) vs. a loss of 1.22% on the S&P 500 as of March 30.

Remember, as bond yields rise, bond prices fall, as do the prices of bond proxies such as utilities, REITs and other high-yielding stocks.

At the same time, the great “Trump Rally” that kicked off after the 2016 election reached a frenetic climax in December and January.

Wall of Worry

The proverbial wall of worry that has characterized the “most hated bull market in history” since 2009 crumbled and was replaced by the fear of missing out, or “FOMO” in traderspeak.

In my opinion, the combination of a surge in bond yields and a sudden preference for high-risk/high-return speculation over slow-and-steady investment caused most income-focused sectors to underperform in January.

And then February happened. Volatility returned with a vengeance, dragging virtually everything down, growth and value alike.

So, in effect, value and income sectors enjoyed none of the benefits of the January rally, yet still took a beating along with the broader market in February and March.

Tech Defanged

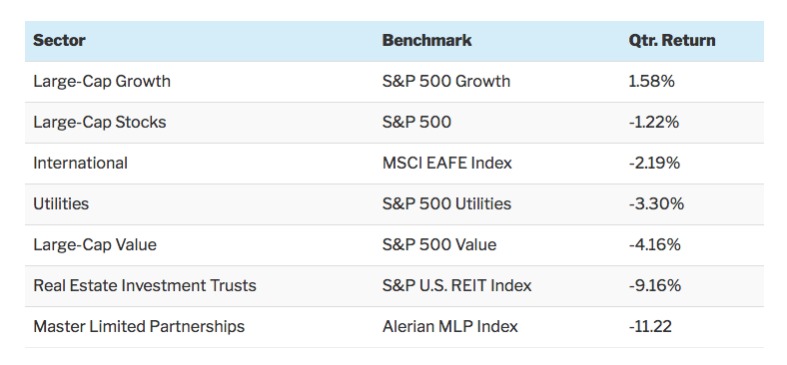

It’s striking to see the differences between sectors. Even after the selloff in the leading growth stocks — the “FAANGs” of Facebook (FB), Amazon (AMZN), Apple (AAPL), Netflix (NLFX) and Google (GOOGL) — the S&P 500 Growth Index still managed to finish the quarter with a 1.58% gain.

Meanwhile, the S&P 500 Value Index — which is a reasonable proxy for Sizemore Capital’s Dividend Growth Portfolio — was down 4.16% as of March 30.

REITs and MLPs — two sectors in which Sizemore Capital had significant exposure at various times during the quarter — were down 9.16% and a staggering 11.22%, respectively.

Suffice it to say, if your mandate calls for investing in income-oriented sectors, 2018 has been a rough year.

Bear Market

I do, however, expect that to change. While I consider it very possible that we see a bona fide bear market this year, I expect investors to rotate out of the growth darlings that have led for years and into cheap, high-yielding value sectors that have been all but abandoned.

They don’t ring a bell at the top. But often times, there are anecdotal clues that a market is topping.

As a case in point, my most conservative client — a gentleman so risk averse that even the possibility of a 10% peak-to-trough loss was anathema to him — informed me in January that he would be closing his accounts with me because I refused to aggressively buy tech stocks and Bitcoin on his behalf.

He wasn’t alone. Again, anecdotally, I noticed that several clients that had been extremely conservative since the 2009 bottom suddenly seemed to embrace risk in the second half of last year. The fear of missing out — FOMO — had its grip on them.

Pricey Stocks

I want to avoid falling into the same mental trap.

Today, the market is expensive by historical standards. The cyclically-adjusted price/earnings ratio — or CAPE — is sitting at levels first seen in the late stages of the 1990s tech bubble.

Meanwhile, we are now nearly a decade into an uninterrupted economic expansion, and we’re effectively fighting the Fed. Chairman Jerome Powell has made it very clear that he intends to raise interest rates fairly aggressively to nip any potential inflation in the bud.

None of this guarantees that the current stock correction will slide into a bear market. (The same basic conditions were true in the 1998 correction, and stocks went on to rally hard for another two years.)

But it does tell me that caution is warranted, and that now — more than ever — I believe we should stick with financially-strong value and dividend stocks.

In a turbulent market, I expect to see investors seek shelter in “boring” value stocks offering a consistent payout. In a market in which capital gains no longer appear to be the “sure thing” they were a year ago, a stable stream of dividend income is attractive.

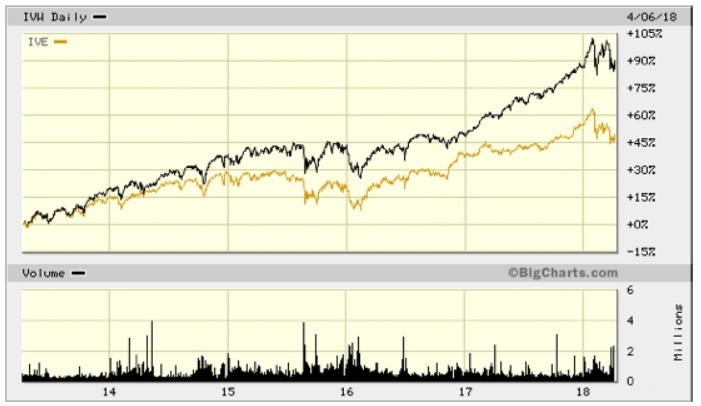

Growth utterly destroyed value last quarter. But this is really just a continuation of the trend of the past five years.

Consider the five-year performance of the iShares S&P Value ETF (IVE) and the iShares S&P 500 Growth (IVW). Growth’s returns have literally doubled value’s, with most of the outperformance happening in 2017.

Growth massively outperformed value in the last five years of the 1990s. But this is by no means “normal” or something that should be expected to continue indefinitely.

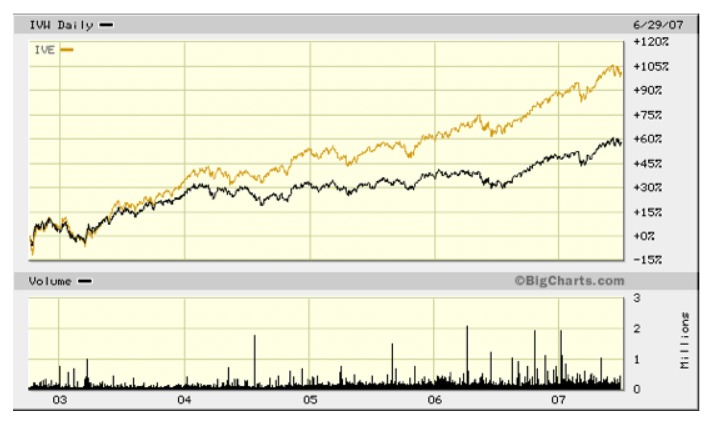

Consider the performance of the same two ETFs in the five years leading up to the 2008 meltdown.

Value stock returns didn’t quite double their growth peers. But they outperformed by a solid 40%, and that’s not too shabby.

Takeaway

This by no means guarantees that value stocks will outperform or that the specific value stocks Sizemore Capital owns will outperform.

But if the market regime really has shifted — and I believe that it has — then the “FAANGs” story is over. Investors will be searching for a new narrative, and I believe that value and income stocks will be a big part of that story.

In the first week of the second quarter, I moved to a moderately defensive posture, shifting about 20% of the portfolio to cash. This gives us plenty of dry powder to put to work once this correction or bear market runs its course. But if I’m wrong, and this is yet another buyable dip, then we still have substantial skin in the game.

And whether the market goes up, down or sideways, we will seek to continue to collect a high and rising stream of dividend income.

Looking to a better second quarter.

Photo Credit: Hamza Butt via Flickr Creative Commons

{kind=link}

{kind=link}