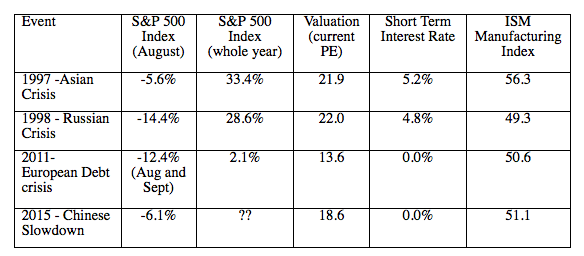

The difficult market environment in August reminded us about three other Augusts–in 1997 (Asian financial crisis), 1998 (Russian default crisis) and 2011 (European debt crisis).

In each of those episodes, there were some type of global risk events. US markets took a hit initially.

Asian Crisis

In 1997, the Asian financial crisis started in Thailand with the collapse of the baht.

That came after the Thai government was forced to cut the baht’s peg to US dollar after exhausting its foreign currency reserves.

As the crisis spread to Indonesia, South Korea and Malaysia, most of Southeast Asia and Japan experienced declining currencies, stock markets crashes and a jump in private debt.

The crisis raised fears of a global economic meltdown. As a result, the US equity market dropped by 5.6% in August of 1997.

However, the US market recovered quickly with a 5.5% rally in September.

Russia

In 1998, the Asian financial crisis reduced demand for crude oil and nonferrous metals, and negatively impacted the Russian exports and foreign reserves.

A series of political missteps and inability to implement a set of economic reforms hit Russian investor confidence and led to capital flight.

Without enough foreign reserve to support its currency, the Russian government devalued the ruble and defaulted on domestic debt on August 17, 1998.

The Russian default caused global liquidity to dry up and credit spreads to widen, which brought down a hedge fund called Long Term Capital Management.

US equity markets tumbled 14.4% in August of that year, but again recovered nicely in September and October.

Euro Crisis

In 2011, the European debt crisis intensified after it started in the wake of the Great Recession around late 2009.

In August of that year, the government bond yields in Italy and Spain breached the 6% level as European leaders struggled to reach an agreement to expand a bailout fund for Greece.

The US equity market dropped by 12.4% during August and September. However, once again, it recovered in October, gaining 10.9%.

China Syndrome

This year, the stock market rout started in China when Beijing unexpectedly devalued its currency, which triggered concerns over a global economic slowdown. The US equity market declined by 6.1% in August.

The equity market drops in the first three crises all recovered nicely and quickly.

Will this time be the same? We believe it is quite likely, though we still recommend caution.

What Crisis?

There is no crisis this time. The Chinese economy has slowed down from double digit rates to round 7%. That is hardly a disaster.

Everyone tends to agree that the world’s second biggest economy will grow at a reasonable pace.

The Chinese stock market rout started after a dramatic run-up in China’s domestic stock markets. The sell-off, though painful, was a necessary correction.

As a word of caution, the bad news from China may not be over. We may see more market volatility going forward.

US Valuations

The US equity valuations are not cheap, but neither are they extreme. During the crises in 1997 and 1998, US stock prices were far more expensive.

The US monetary policy is ultra-loose. Even if the Fed raises interest rates this year, the monetary policy is still very accommodative. The interest rates in 1997 and 1998 were much higher.

American Economy

The US economy is solid. In Q2, the US economy grew at 3.7% annual pace. ISM Manufacturing Index is still in expansion territory and unemployment rate is close to 5%.

The slowdown in China will have limited impact on US growth as exports to China only account for 1% of the GDP in the US. However, the slowdown in China will have significant impact on US companies that are doing businesses there.

Photo Credit: Lue Huang via Flickr Creative Commons