Tax benefits from corporations re-domiciling into lower tax rate geographies, known as tax inversions, appear to have accelerated M&A activity.

Pfizer’s (PFE) attempt to purchase AstraZeneca, Omnicom (OMC) merging with Publicis (PUBGY), and Salix Pharmaceuticals (SLXP) acquiring Cosmo Technologies are all examples where the newly combined entity will be headquartered in the home country of the acquired company, which is intentionally outside of the United States.

One of the attractions of these acquisitions is to implement a strategic tax inversion, whereby the newly formed company will be subject to the lower tax rate of its foreign constituent.

This results in increased margins and higher corporate earnings while decreasing the U.S. tax collections.

The World is Flat

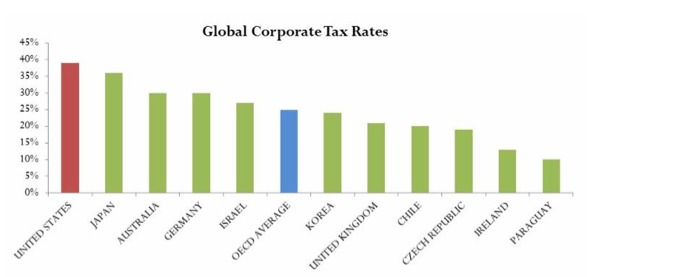

U.S. domiciled corporations pay a 39% tax rate, while the average corporate tax rate for industrialized countries is 25%. In order to remain competitive in the world economy, some U.S. companies are implementing strategies to mitigate the tax rate differential.

Several countries have particularly low corporate tax rates and, not surprisingly, they have been targeted locations for a corporation to move to or merge with another corporation. Bermuda, the United Kingdom, and Ireland are among the most tax efficient locations for American corporations to re-domicile.

Most industrialized countries employ a territorial tax system, which means that corporations only pay taxes on income earned in that specific country. France, Germany, England and Hong Kong utilize the territorial tax system, while the U.S. does not.

U.S. companies are required to pay taxes on the difference between the U.S. tax rate and the international tax rate in order to repatriate profits earned in international markets.

As a consequence of this tax law, U.S. companies keep more than two trillion dollars of corporate profits overseas to avoid the incremental tax burden. This capital can only be used for international investments – acquisitions or capital expenditures – and cannot be returned to the U.S. without incremental tax payments.

Inversion strategies

There are two different inversion strategies most commonly utilized by U.S. companies. First, corporations are moving their headquarters abroad to countries with a lower tax rates.

In 2009, Ensco Plc (ESV) moved its headquarters to the United Kingdom without transferring a significant number of employees from the U.S. By the first quarter of 2014, Ensco was able to reduce its tax rate to 14% from the 27% it paid in the last quarter before it re-domiciled.

Second, US companies are merging with foreign companies to benefit from the foreign entity’s lower tax rate. In 2013, Actavis (ACT) acquired Warner Chilcott (WCRX), an Irish pharmaceutical company.

The post-merger entity dropped its tax rate from 33.6% in the fourth quarter of 2012 to 17% in the second quarter of 2013. More than 50 U.S. companies have reincorporated through inversion in the last 10 years with most of them completed since 2008.

Congress is considering tax laws changes to minimize the re-domiciling trend and avoid losing tax revenue. Current tax policy states that a corporation can only qualify for tax inversion if at least 20% of its shares are held by a foreign company.

For the 2015 budget, the White House proposed increasing the necessary ownership of the foreign entity to 50% in order to make inversion driven M&A more difficult. Longer term, there is increasing interest in comprehensive tax reform.

Among the proposals being floated in Washington include:

- Reducing the corporate tax rate to a rate closer to the OECD average and removing loopholes.

- A one-time tax holiday to repatriate overseas profit. This was implemented in 2004 and proved relatively ineffective.

- Convert the U.S. to a territorial tax system.

No Tax Reform Until 2016

Despite the recent increase in companies that are creating tax inversions it is unlikely that any tax reform will take place prior to the 2016 election. Tax reform will probably be one of the major areas of debate during the election.

While both Democrats and Republicans appear to agree that tax reform should occur, there is no agreement across parties or even within parties regarding strategy and direction.

In the meantime, there is greater awareness about the spread of tax inversions and a growing concern about the impact on U.S. tax collections.

Walgreens recently surprised investors by announcing that the company will not execute a tax inversion even though they are buying UK based Alliance Boots early next year. Press reports and comments from Walgreen’s management suggest that the company was worried about a negative public reaction that could lead to customer boycotts and the potential for an extensive and difficult IRS review of the transaction.

How to Play It

- M&A Activity: Redwood anticipates that merger activity could continue at an accelerated pace as U.S. companies strive to complete acquisitions that enable tax inversion before tax reform is implemented. Companies with significant U.S. operations but domiciled in low-tax rate jurisdictions would continue to be attractive acquisition candidates.

- Redeployment of Capital: Tax reform could create an opportunity for the cash trapped overseas to become available for dividends, buybacks and capital expenditures. Companies with strong balance sheets could provide positive capital redeployment surprises for shareholders.

- Higher EPS from Lower Taxes: Comprehensive tax reform could lower tax rates for companies with disproportionately high tax rates. These companies could experience material tax burden reductions resulting in higher earnings and cash flow, which could have a positive impact on their stock price.

Photo Credit: Taxcredits.net, Flickr Creative Commons

DISCLAIMER: The investments discussed are held in client accounts as of August 31, 2014. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.

{kind=link}

{kind=link}