The debate over whether the U.S. Federal Reserve should start tapering its $85 billion a month of bond purchases breaks down into two big camps: Those who criticize Ben Bernanke for using the central bank to distort market pricing, and those who think he’s about the only guy standing in the way of an even weaker recovery.

In a way, the arguments hardly matter at this point. Investors have already started to price in a Fed wind-back of its quantitative easing program — and that’s having a negative impact on the housing market and emerging markets.

In July, new homes sold across the country fell 13.4% compared with the previous month, the biggest decline in more than three years according to government data.

Economists blamed rising mortgage rates, driven higher by speculation on an impending Fed taper. The benchmark 30-year fixed-rate mortgage rose to 4.74% from 4.57% percent last week, according to the Bankrate national survey of large lenders. That’s the highest level in two years.

US 30 Year Mortgage Rate data by YCharts

One of the goals of the Fed’s QE program in the first place was to revive the scorched housing market. Now, with that slipping away, Ed Yardeni points to an intriguing idea that was kicked around at the recent Jackson Hole gathering of economists and central bankers:

The talk of the town at this past weekend’s Jackson Hole monetary policy conference was a paper presented by Arvind Krishnamurthy and Annette Vissing-Jorgensen on Friday… the two academics argued that the Fed should taper its purchases of US Treasuries while increasing its purchases of mortgage-backed securities. That certainly is a novel variation on the QE tapering theme that has been unsettling financial markets since May 22, when Fed Chairman Ben Bernanke first raised the subject.

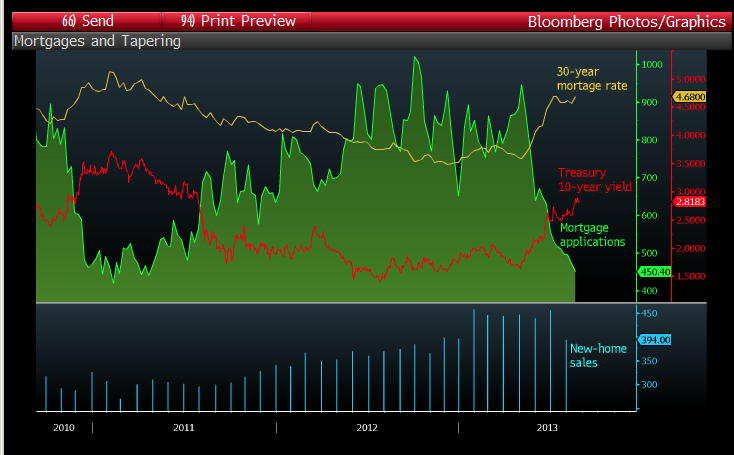

One disturbing trend that Bloomberg points to is the big downturn in mortgage applications. Check out the next table:

Time to panic? Nonsense, say Fed critics like the American Enterprise Institute’s Edward Pinto, who argues the Fed has created an environment of artificially low interest rates that’s inflating another housing bubble. Better to withdraw support and let pure market forces shape the home market, says Pinto:

While a housing recovery of sorts has developed, it is by no means a normal one. The government continues to go to extraordinary lengths to prop up sales by guaranteeing nearly 90% of new mortgage debt, financing half of all home purchase mortgages to buyers with zero equity at closing, driving mortgage interest rates to the lowest level in 100 years, and turning the Fed into the world’s largest buyer of new mortgage debt.

Meanwhile, liberal pundits like economist Paul Krugman think the Fed should move very cautiously and that primary cause of recent financial bubbles hasn’t been Fed policy, but rather lax regulation over Wall Street:

O.K., the other obvious culprit is financial deregulation — not just in the United States but around the world, and including the removal of most controls on the international movement of capital. Banks gone wild were at the heart of the commercial real estate bubble of the 1980s and the housing bubble that burst in 2007. Cross-border flows of hot money were at the heart of the Asian crisis of 1997-98 and the crisis now erupting in emerging markets — and were central to the ongoing crisis in Europe, too.

The big sell-off in Asia currencies (notably those of India, Brazil and Indonesia) started in May, right around the time the Fed started to hint it might reverse course. Some analysts suggest the currency turmoil reflects the flow of hot money back to the U.S. now that rates might be heading up.

Another sign that emerging market stock investors are rushing to the exits: during the first half of 2013, investors pulled $13.9 billion from equity mutual funds that are invested in these four countries, according to EPFR Global.

{kind=link}