A fiscal cliff deal now looks impossible; anything that might spring up this week will likely be just a stopgap measure in our opinion. We had some hope earlier, as we felt our country’s best interests were finally aligning with Washington’s. They wanted to get home for Christmas, New Year and family vacations, and the country needed a fiscal deal to keep from crashing on the rocks. We never felt anyone would get a real “conscience” and do what’s right for the country, just that they would do whatever they could to get on vacation.

But let’s face it, the phrase “leadership in Washington” has officially become an oxymoron. The typical deal is fought for TV face time, marketing sound bites and general selfless promotion – nothing remotely magnanimous, nothing for the good of God and Country. There are 535 elected members of Congress in the two houses. Throw in two elected executives and you have 537 people supposedly “leading” our country. So far none of them seems remotely qualified for a leadership role and had they been at the helm of a major corporation, they’d have been fired long ago. The only bipartisan thing about Washington these days is the total amazement of how badly broken the system seems to be.

This incredible cliff episode now looks to be the topic of the new year. We think the questions like how, when, and if the problems get handled responsibly will continue to haunt us throughout 2013. Add in the ObamaCare investment taxes and what we see as the inevitable unintended consequences flowing from 2000 pages of legislation and we believe we will surely encounter a stumbling block or two.

We believe the penalties for going off the fiscal cliff – mandated taxes and spending cuts – are clearly not a recipe for growth, and perhaps even a good prescription for a recession. In some respects they may be preferable to what Congress has demonstrated they are capable (or incapable) of producing on their own. Maybe the right thing to do is to take the pain, work through it, and then get on with things.

Prognostication

Much is riding here on the details of any fiscal cliff agreement, so predicting 2013 is a bit of a crap shoot. But it’s year-end, so here we go: our review of some of thoughts from 2012 and some ideas for the major asset classes in 2013.

Domestic Equities

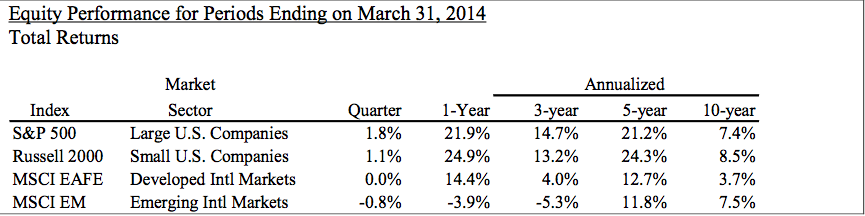

Last year we said that “salt of the earth, rock solid, large moat, dividend paying, cash flow generating stocks are OCM’s asset of choice for 2012. We like companies that have large hoards of cash, competitive staying power and possibly a better credit rating than the USA.”

Using the Dow as a proxy, this asset class did reasonably well, enjoying a total return (factoring dividends paid as re-invested into the index) of over 10% for 2012. Some of our choices clearly did better than others: Wal-Mart (WMT), for example, enjoys an approximate 18% total return year to date. Intel (INTC), down about 15% in 2012, was a notable disappointment. However, we believe Intel is likely now to get a boost from Microsoft’s introduction of Windows 8.

Going forward, we continue to favor this sub-asset class, as it still appears relatively under-loved, not as accepted as bonds overall and not as risky as the now popular high yield (remember, “junk”) bonds. These companies generally pay us better than Treasuries do to be a shareholder in some of the best businesses around. The 12-month calendar is probably not the best way to judge these companies, as we tend to take a much longer view, but knowing we have stakes in what we believe to be some of the world’s best run businesses helps us sleep soundly at night. The percentage stake we hold here will not go down and will very likely increase.

Gold

We said last year at this time: “Our global/macro perspective on Gold just hasn’t changed despite the decade-long rally. Things are just not looking good in Europe (or the USA for that matter) regarding debt levels of both key financials and sovereigns. The only logical way out will be for the various sovereigns to continue printing money to pay for everything and we see that as supportive of Gold prices.”

Gold, as of this writing (12/24/12), has logged another year in the plus column with a “simple” (given it pays no dividends or interest that can be reinvested) return of 2.40 %. That’s clearly not spectacular, when compared to other assets, but given the sad state of global affairs, it’s part of a defensive strategy we felt it best to play and therefore own a significant position. Gold had many closes above $1700 an ounce this year and helped us hedge away some of our exposure to other dollar denominated assets.

In 2013, in the global landscape just doesn’t look terribly different to us: We believe government spending will continue unabated, the currency printing presses will continue to run amok, and the hard decisions that need to be made by global politicians will continue to be sidestepped. We fear the genie is getting further out of the bottle and persuading people to give back government handouts will be difficult, at best. This is typically not ground political officials like to touch, and we feel they rarely make the right or hard decisions. Our fear is, in an attempt to spur exports and economic growth, this will spiral into a “beggar thy neighbor” currency policy. This strategy could easily be deemed the only logical way out of massive and growing debts. We believe the solution by default will be to devalue the respective currencies either by mandate or straight inflation.

So we still feel strongly about a significant allocation to gold, and we have only partially altered or adjusted our view by allocating some of our allotment to the underperforming major gold mining companies. As we have said in the past, we don’t appreciate the often-volatile periods gold goes through, the result – all too frequently – of margin clerks selling gold as the easiest and most liquid asset. Remember, these types aren’t judged by their asset selection skills when trying to cover a “hole” in someone’s account, but rather by how quickly that “hole” is covered. Liquid markets like gold can help those clerks make up lost ground in a hurry.

European Equities

Last year we were a bit nervous about this asset class, and said we “suspect we at OCM will keep things about unchanged without any deepening allocation. However, remember the problem in Europe is that we are still in the ‘word stage.’ If positive deeds start occurring, or when the markets stop the violent down trades on bad news, we may look to change things here slightly by increasing the allocation.”

In 2012, this asset class had a total return of over 14%, as measured by the EAFE Index Fund (EFA), so it fared significantly better than we expected, even though we had our suspicions.

The noise this year has been sounding much better than before, and the talk of both a banking and eventually a fiscal union of sorts makes tremendous sense. But now we wait for the actual delivery, and that may take some time. Initially it sounded like the end of the year for some semblance of a blueprint for the banking union to develop, but now it seems more like early next year.

The ECB ‘s Mario Draghi took a stand for the Eurozone this summer and managed to put a floor under the Euro at around 1.20 US dollars per Euro. All in all, it seems like real recovery is in the offing and we believe some type of reform will begin this year in earnest. We believe adding to this sub-asset class, or rather bringing our exposure to international equities to a higher percentage of its maximum allocation, is likely a good way to go.

Emerging Market Equities

In January we said about the emerging markets: “Over the years, the emerging markets often significantly outperform, both on the upside and the downside. We can easily see increasing our allocation a bit here as things begin to get a little better. Our feeling is that a few of these countries will respond quickly and well to any sort of pickup in economic activity in the USA, even just a moderate base line growth level should help them get their footing. This should help them regain their leadership role in the global growth race.”

Using the MSCI Emerging Markets Index as a barometer, the total return for EM equities so far this year has been just over 16%, as of December 24. That’s impressive but really not much different than the S&P 500, at 16% gain to date (total return, as of 12/24/12). Considering the increased level of risk, we would have expected this asset class to outperform more convincingly, given the general bullishness that prevailed for the S&P.

In 2013, assuming some version of avoiding the US fiscal cliff, and given general sentiment about US equities, we would expect EM equities to continue to outperform and believe we will bump up our exposure a notch in 2013.

US Treasuries

In January we wrote “Next year what do we expect? Hey, a 1.50% ten-year note doesn’t sound that far-fetched after all, and given our current World-in-Crisis mode and the Fed’s desire to bring down long term interest rates, maybe it’s not too crazy to expect ten year notes to hit 1.25 to 1.50%.”

Given that we were dead wrong in 2011 (although we had plenty of company – even the “bond-savant“ himself, Bill Gross, got it wrong), last year was pretty much a direct hit for OCM. By mid-year the yield on the 10-year note touched below 1.40%, exactly as we had called.

We find the following long term chart of the generic 30-year US Treasury quite revealing.

Chart: Bloomberg

The yield on the generic 30-year US Treasury has declined – so the price has gone up – for about 32 years. We think that’s a pretty good run for bonds overall, and we believe logic would soon have to prevail as rates will not likely go negative.

As a point of fact, all calculations done for US bond performance and their various correlations have about 30 years of data that reflects a gigantic one way movement. We believe this is highly unlikely to continue, given the current levels of inflation around 2% (November Consumer Price Index was 1.90% year-over-year) – that nets out to real yield of just 1% for 30 years!

As a result, this isn’t our favorite asset class at this point, so now what? Many of us know John Maynard Keynes once said, “The market can stay irrational longer than you can stay solvent.” We are not here to try and catch falling knives either, but the point of an asset allocation strategy is to take yourself out of the market timing game. Thinking you will be able to maximize your exposure to the best performing asset class on a regular basis is just a fool’s game, and inconsistent with a longer term approach to portfolio management in our opinion. The point is to have some exposure to multiple asset classes, so when the next regularly scheduled Black Swan shows up, we will be ready to capture the next “risk-off” movement.

Oil & Gas

Last year we commented, “Oil seems like it will vacillate from crisis to crisis, whether it’s due to a lack of refining capacity, continuation of the Arab spring uprisings, or Iran’s closing the Straits of Hormuz. Natural gas seems to be well supplied, with new discoveries coming out of the U.S. constantly. The U.S. shall soon be a net energy exporter again.”

Using XLE, the Energy Select Sector SDPR, as a gauge, this sector’s total return was around 4% in 2012.

Chart: Bloomberg

The 5-year chart of WTI crude (above) suggests to us that crude will likely maintain its slow steady rise, although there is no shortage of people who believe this commodity is about to break down. With all the unknowns in Syria, Iran, Egypt, Nigeria – or for that matter the potential roadblocks to more drilling here in the USA – we feel the long term global energy needs will keep a floor under this market. Natural gas seems to be trying to level off and put in a bottom here. The 70% move down over the last 5 years seems to have run its course; we feel the natural laws of supply and demand will keep a floor in Natural Gas as well.

Forex

Last year we commented “The dollar seems to hold its negative correlation in times of crisis very well as the short-dated T-bill market gets a strong bid and the dollars follow. It provides a nice offset to declining equities prices, but in lower interest rate environments there is a floor on how much Treasuries can rally, whereas the dollars could continue to rise. We are cautious on FX assets right now.”

That was probably not as clear as we should have been, but the dollar, as measured by DB US Dollar Index Bullish Fund, was off over 3.00%. We feel that, as far as a hedge against declining equity prices – given the global propensity to run to US T-Bills – the USD is not a bad hedge. It moves the same way as T-Bills in a crisis and at least doesn’t have a built-in floor. It’s not impossible for T-Bills to have negative returns (although for extended periods of time this is unlikely to happen) where the dollars versus the Euro (for example) has no defined natural level of resistance.

If anything, given the real levels of return for US Treasuries, we would be more apt to move into Dollar bullish trades as a defensive trade for our portfolios, than worry about missing the incremental “interest” earned by being long US Treasuries as a defensive play. Additionally, when interest rates start up again, we believe the move into dollars should be magnified, as demand for dollars increases due to the higher interest rates.

Real Estate & Alternative Assets

In 2012 real estate also had an excellent return, considering the Vanguard REIT ETF, VNQ, as a market proxy – it’s total return was approximately 17.00%, on par with the return of S&P 500 Index. We think the Real Estate situation has gone “from worse to bad” – that is, getting better. This is the time we are likely to look seriously at adding here – when things look truly to be on the mend. The early returns have been made, and we are looking for a way to leverage Real Estate and enjoy what looks to be its brighter future.

Wrapping up

Finally, worthy of note this year has been the high correlation across many asset classes – particularly domestic, international and emerging market equities. Even gold and bonds managed a positive return in this calendar year. We think this a bit strange, and are rethinking our bond allocation given its historic performance, particularly since the yields on bonds are now so low.

We will, of course, stay diversified across multiple asset classes, and keep bonds primarily for disaster insurance, or black swan type trades, but wonder how much protection they can offer a such low real interest rate levels. We clearly are in uncharted waters in this regard, and may find ourselves more comfortable moving some of our bond allocation to the FX (USD Bullish) model. The idea is to have a potential level of protection while not bumping up against real “inflation adjusted” interest rates approaching zero.

The investments discussed are held in client accounts as of November 30, 2012. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.

Certain investments discussed in this presentation are for illustrative purposes only and there is no assurance that the adviser will make any investments with the same or similar characteristics as any investments presented. The investments are presented for discussion purposes only and are not a reliable indicator of the performance or investment profile of any composite or client account. Further, the reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions made by model managers in the future will be profitable.

Certain information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The manager believes that such statements, information and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}

{kind=link}