Manager: 401 Advisor

Manager: 401 Advisor

Model: Dividend and Income Plus

Our Dividend and Income Plus model‘s objective is for a long term return commensurate with the S&P 500, with lower risk (beta) and a higher yield. To accomplish this the strategy has two components: a high dividend stock component and a trading component that trades the SPDR Barclays Capital High Yield Bond Index ETF (NYSE: JNK).

JNK serves two purposes. The first is to provide a higher yield to the portfolio as high yield corporate bonds typically offer a substantially higher yield than can be found in most stocks. The second purpose is to provide capital gains. The objective here is to sell and go to cash when yield spreads between high yield bonds and treasuries begin to widen (higher yields mean lower prices) and to buy back when spreads top out. We then aim to ride the narrowing spreads back down, collecting nice dividends and capital gains along the way.

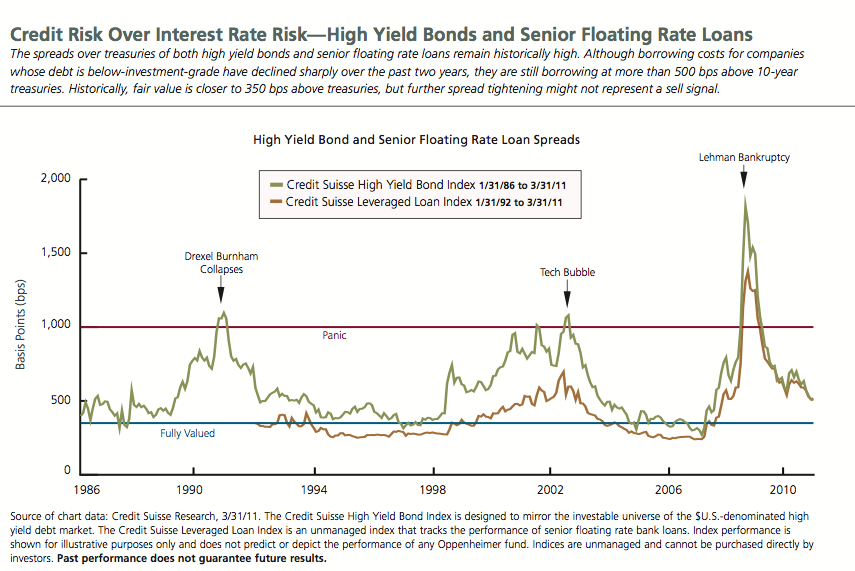

As the graph below from Oppenheimer Funds shows, high yield bond yield spreads are approaching historic lows relative to treasury yields. With JNK yielding just 8.55% as of 5/3/11, this position is adding little to our yield target of 8%, barely enhancing our yield. Second, it doesn’t appear that JNK will provide us with significant capital gains before a JNK spread widening cycle begins and forces us to cash, losing its yield contribution entirely.

Our strategy for the foreseeable future then, is to bring up the yield on our stocks to compensate for JNK. We are also worried about inflation and the impact it could have on typical dividend payers like REITs and Financials. Our current holdings have an indicative yield of 7.48% as of May 10th (data from Covestor*).

For May we will be selling our position in Penn West Petroleum (NYSE: PWE), as its yield of 4.27% (as of 5/4/11) doesn’t warrant holding. While it is a Canadian energy play, we feel that the run in oil prices has neared its peak.

Similarly we are selling ONEOK, Inc. (NYSE: OKE) with a current yield of just under 3% (as of 5/4/22).

Look for new holdings over the next several days as we do not want to keep a large cash position in this current market. Overall we expect that the model’s yield will fall to the 7% range over the summer. But with the bull looking to still have legs, we’ll sacrifice a little bit of yield for better capital gain prospects.

Sources:

JNK Yield from FinViz.com: http://finviz.com/quote.ashx?t=JNK

High-yield bond spreads: “Capital Markets Perspectives as of 3/31/11” OppenheimerFunds, 3/31/11. Page 15. https://www.oppenheimerfunds.com/digitalAssets/FINAL_CMP_Chart_Book_063010-0dc31c53-7fb1-4128-a7f1-746c59988662.pdf

Chart data: Credit Suisse Research, 3/31/11.

*Note: Indicative yield is calculated the last known dividend, divided by the current price, and is shown annualized. It is therefore sensitive to price movements and does not represent a promise of income or total return over the next 12 months. Raw data was obtained from Bloomberg, calculations by Covestor.

{kind=link}