With earnings season starting to wind down, it’s becoming clear that this has been one of the best corporate reporting periods in years, in my opinion.

With nearly 81% of companies in the S&P 500 reporting results through May 3, almost 77.5% have beat earnings estimates, while almost 17% have missed.

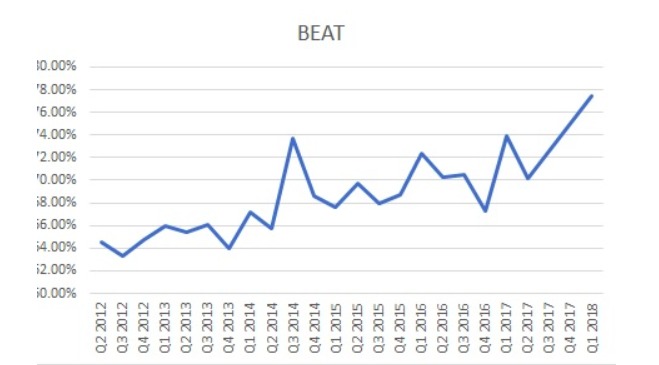

I compiled the charts below from data from Dow Jones S&P Indices, and they show that, to this point, this has been by far the best quarter when it comes to companies beating expectations since 2012.

Robust Earnings

According to Dow Jones S&P, 303 of the 405 companies reported so far, have beat on sales estimates as well.

Sales in the first quarter are estimated to have risen by nearly 10 percent, making this quarter more than just about the bottom line.

Earnings for the full year in 2018 are forecast to rise to $153.06, and $170.48 in 2019. It leaves the S&P 500 trading at 17.4 times 2018 estimates and only 15.6 times 2019 earnings estimates.

According to Dow Jones S&P, 303 of the 405 companies reported so far have beat on sales estimates as well.

Sales in the first quarter are estimated to have risen by nearly 10 percent as well, making this quarter more than just about the bottom line.

Looking Ahead

Earnings for the full year in 2018 are forecast to rise to $153.06, and $170.48 in 2019. It leaves the S&P 500 trading at 17.4 times 2018 estimates and only 15.6 times 2019 earnings estimates.

Even with the rising interest rate scenario, investors have become concerned with the ratio of the 10-year Treasury yield to the S&P 500 yield, is only at 1.56.

In other words, this means that the 10-year yield at 2.95 on April 30 is 1.56 times more than the S&P 500 yield of 1.89 percent.

The average ratio since 1962 is 2.19 with a standard deviation of 0.86, a range of 1.32 to 3.05. So the S&P 500 is still on the cheap side of the historical average, and the historical norm.

Takeaway

In my view, it is clear from the chart above that in late 1990s and early 2000s, which saw the ratio explode as the stock market soared, just how overvalued the market was to bonds at the time.

So at this point, yields would have to rise a lot further.

It would take yields on the ten-year to reach 4 percent to get to the historical average, according to my research.

For now, in my view, it continues to be tough to say that stocks are overvalued to earnings or bond yields.

Photo Credit: 401(K) 2012 via Flickr Creative Commons